How to backtest a trading strategy (the complete method)

The method for backtesting a strategy seriously: sample size, unambiguous rules, biases to avoid, and moving on to replay.

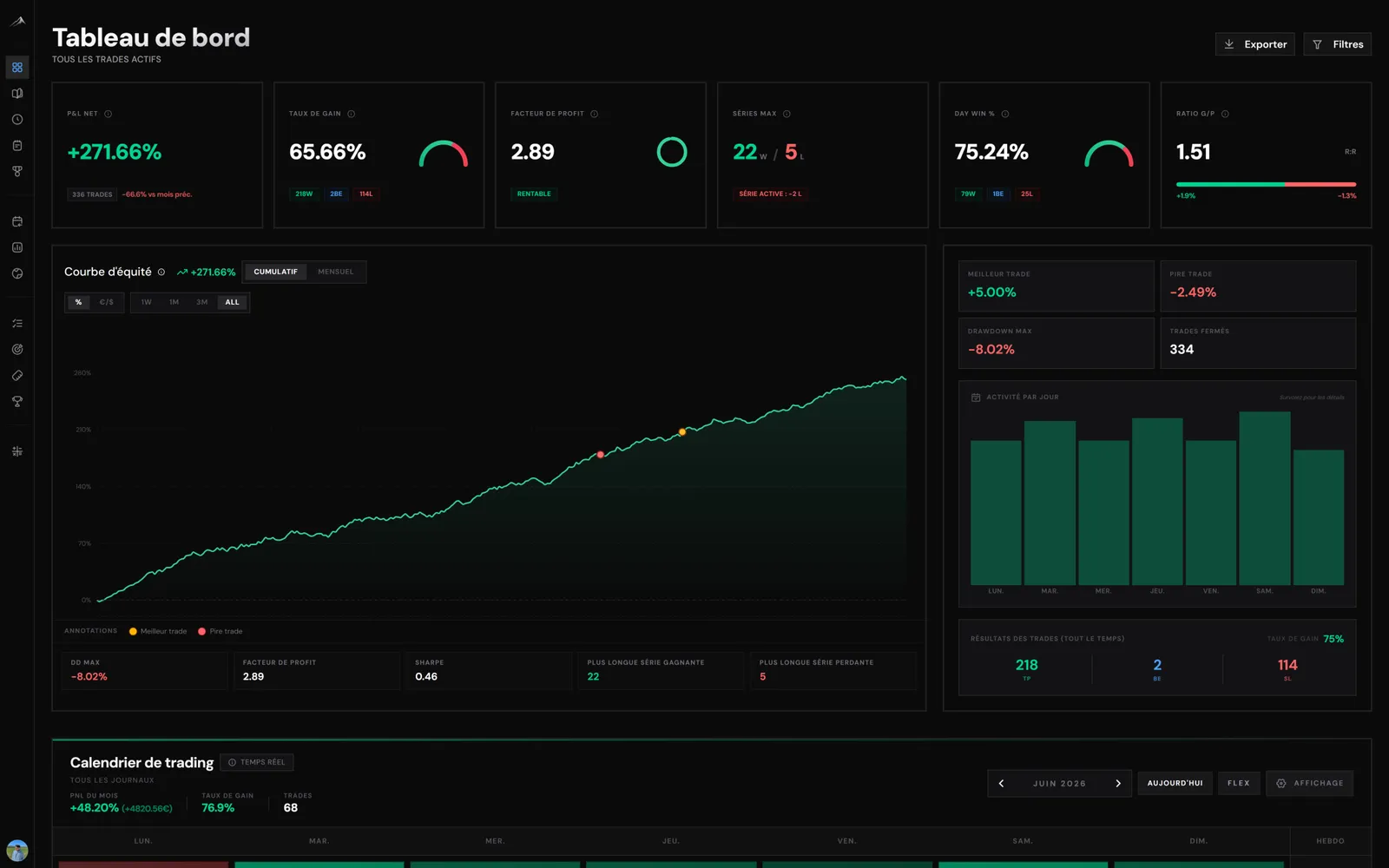

Backtesting means measuring whether a strategy has a statistical edge before you risk real money. Done badly, a backtest breeds false confidence; done well, it saves you months of losses.

1. Define objective rules

A backtestable strategy leaves no room for interpretation: entry conditions, exit conditions, position size and stop management must be written down in black and white. If two people cannot reach the same result, it is not testable.

2. Build a large enough sample

Ten trades prove nothing. Aim for at least 100 trades, ideally spread across different market conditions (trending, ranging, high volatility). An edge that only works in one market regime is not reliable.

3. Avoid the classic biases

- Survivorship bias: don't test only the periods that suit you.

- Overfitting: a strategy tuned perfectly to the past usually fails in the future.

- Hindsight bias: don't cheat by using information you would not have had in real time.

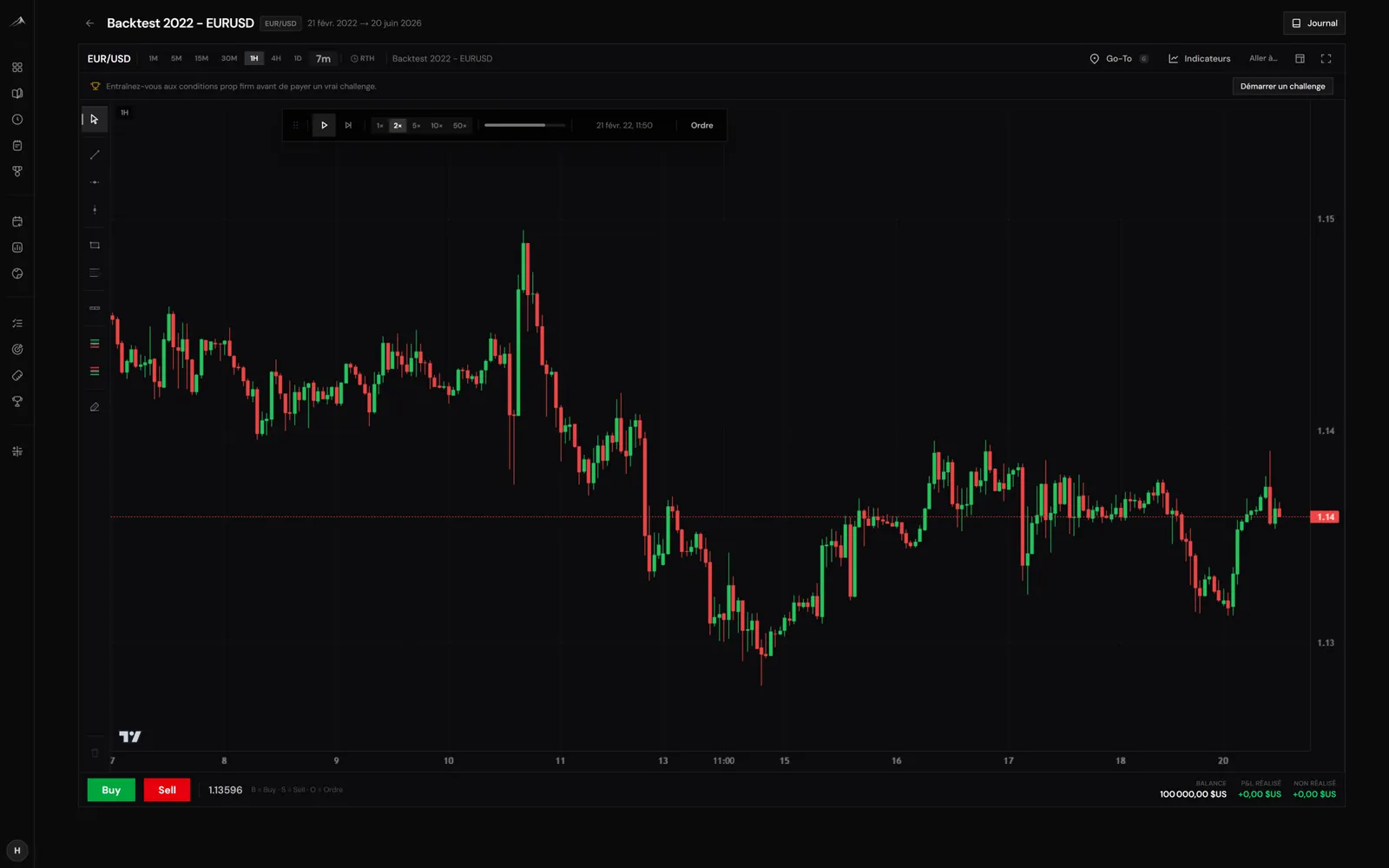

4. Move on to replay

A historical backtest must be confirmed by bar-by-bar replay, which recreates decision-making under realistic conditions. That is exactly what Altiora's backtesting and replay module offers, with journal and analytics built in — see the features.

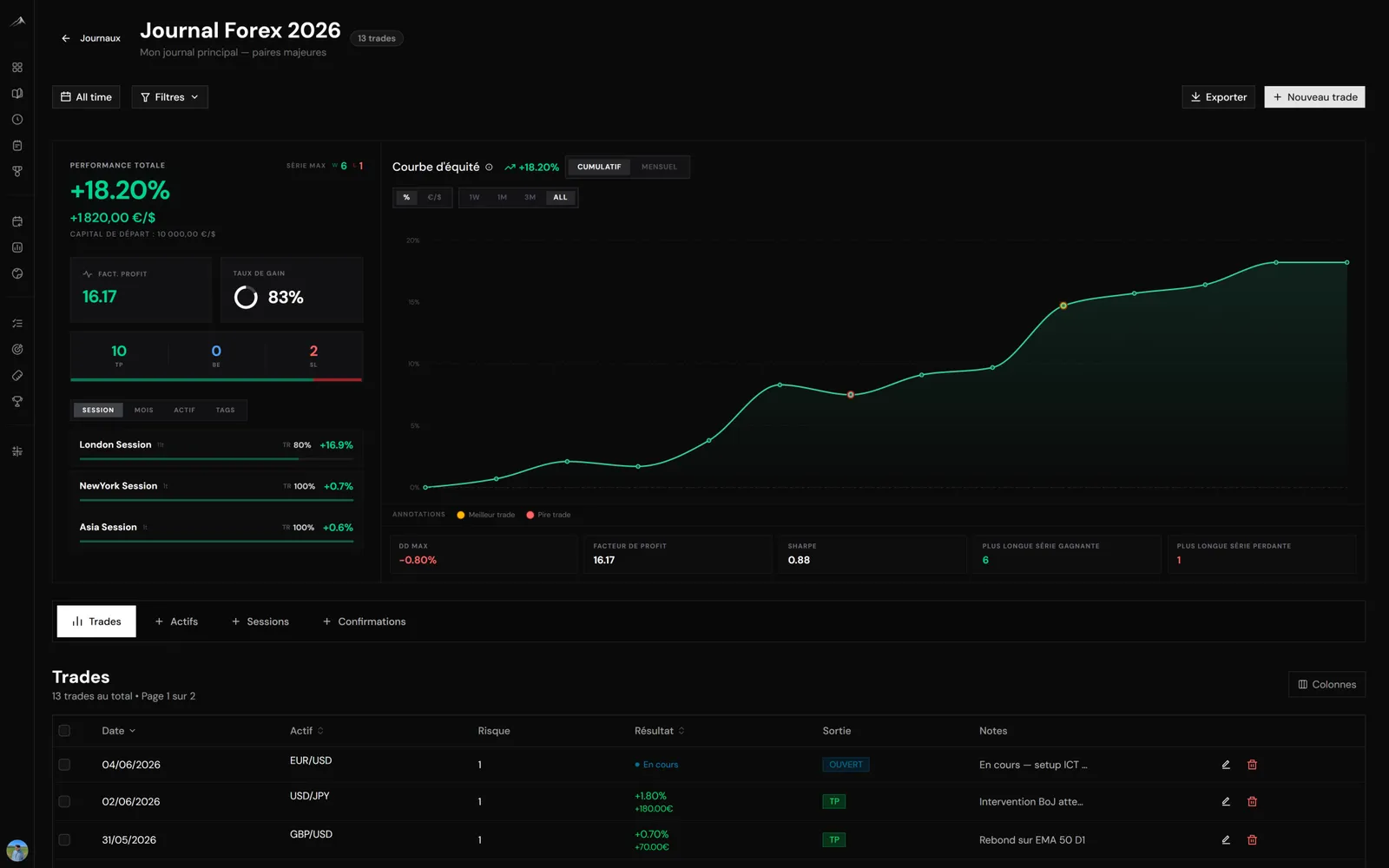

5. Journal your backtests

Treat your backtests as real trades: log them, measure expectancy, compare setups. The logic is the same as in the trading journal guide. Try it for free.